Imagine you are driving home on a rainy Tuesday evening. You glance down for a split second, traffic suddenly stops, and you rear-end the car in front of you. It triggers a multi-car accident. Two people are seriously injured, requiring extensive surgeries and months of missed work.

Within weeks, the medical bills and legal demands total $750,000.

You feel awful, but you breathe a sigh of relief because you have “good auto insurance.” But then you look at your policy’s declaration page and notice your bodily injury liability limit caps out at $300,000.

Who pays the remaining $450,000?

Without a safety net, that money comes directly out of your retirement accounts, your home equity, and your future wages. This is exactly where Umbrella Insurance steps in.

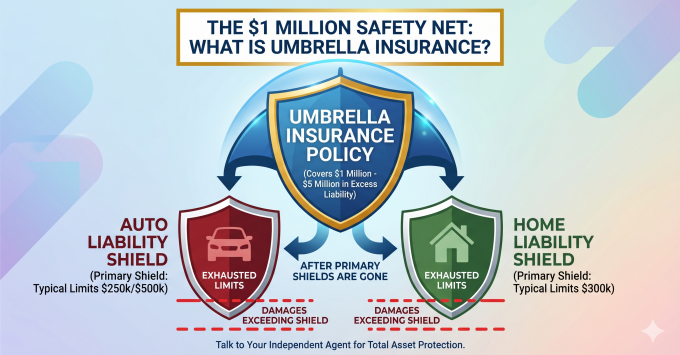

What is Umbrella Insurance?

Think of your standard auto and homeowners insurance policies like primary shields. They protect you up to a certain dollar limit. An umbrella policy is an extra layer of liability protection that sits on top of those shields.

When a catastrophic accident occurs, and your primary auto or home liability limits are exhausted, the umbrella policy steps in to cover the rest, up to your chosen limit (usually starting at $1 million).

Furthermore, it doesn’t just pay the damages; it also covers your legal defense fees, which can easily rack up tens of thousands of dollars before a case even goes to trial.

The Biggest Myth: “I’m Not a Millionaire, So I Don’t Need It”

Many people assume umbrella insurance is an exclusive luxury item for the ultra-wealthy. In reality, it is designed to protect what you accumulate over your lifetime.

A judge or jury doesn’t check your current bank account balance before awarding a settlement. If you are found liable for a major accident, your future wages can be garnished for years to come. If you own a home, have a retirement fund, or have a steady income, you have assets worth protecting.

The Everyday Risk Factors

You don’t have to be reckless to face a massive lawsuit. Common, everyday situations that drastically increase your liability exposure include:

- Having a Teenage Driver: Statistically, teens are involved in more accidents, and as the parent, you are financially responsible.

- Owning a Dog: Even the friendliest dogs can bite if startled. A single dog bite claim can easily spiral into six figures for medical and psychological trauma.

- Having a Pool or Trampoline: Your backyard becomes an “attractive nuisance” in legal terms. If a neighborhood kid gets hurt on your property, the liability falls squarely on you.

- Hosting Social Gatherings: If a guest leaves your holiday party or summer BBQ intoxicated and causes an accident on the way home, you could face a social host liability lawsuit.

The Best Part? It’s Incredibly Affordable

Because umbrella insurance only kicks in after a major primary policy limit is breached, the risk to the insurance company is relatively low. Because of that, the cost to you is surprisingly small.

The Cost Breakdown: A typical $1 million umbrella policy costs between $150 and $300 per year (about $15 to $25 per month). Adding a second million usually costs just a fraction more.

For the price of a couple of streaming subscriptions, you can entirely eliminate the risk of a freak accident wiping out your life savings.

How to Get Covered

To qualify for an umbrella policy, insurance companies will require you to carry certain minimum underlying limits on your auto and home policies (usually $250,000/$500,000 for auto bodily injury and $300,000 for home liability).

The easiest and most cost-effective way to set this up is to bundle your auto, home, and umbrella policies with a single independent agency. This ensures there is no coverage gaps between your primary shields and your umbrella safety net.

Are you exposed? Take five minutes to pull up your current insurance policies and look at your liability limits. If you’re ready for a quick, zero-pressure coverage checkup to see how an umbrella policy fits into your financial plan, call or email our office today.